Financing Restaurant Equipment The Definitive Guide

Getting the right kitchen equipment is a huge hurdle for any restaurant owner, but it doesn't have to drain all your cash. Financing restaurant equipment is how you get the ovens, coolers, and prep stations you need now by using loans or leases. This keeps your cash free for day-to-day essentials like inventory, payroll, and marketing.

Think of it this way: your kitchen is the engine of your business. Financing is the fuel that gets it running.

Why Smart Equipment Financing Fuels Restaurant Growth

Every great restaurant runs on more than just killer recipes—it runs on reliable, efficient equipment. Those high-capacity ovens, walk-in coolers, and stainless steel prep tables are the true backbone of your operation. Upgrading or replacing them isn't just another bill to pay; it's a direct investment in your kitchen's productivity, consistency, and ultimately, your bottom line.

But let's be real, the upfront cost can be a knockout punch. A new commercial range can easily run you $10,000, and a walk-in cooler can blow past that. Paying for these big-ticket items with cash can wipe out the reserves you desperately need for buying ingredients or just making payroll. This is where smart financing becomes a game-changer, not just a last resort.

The Growing Demand for Modern Kitchens

The push for high-quality equipment is everywhere. The global market for restaurant equipment was valued at around USD 92.89 billion and is expected to climb to USD 206.07 billion by 2035. That's not just a random number; it signals a clear trend that modern, efficient kitchens are essential to stay in the game. You can dig deeper into this market expansion at Market Research Future.

By financing, you can get your hands on state-of-the-art equipment without that crippling upfront expense. It gives you the power to:

- Preserve Working Capital: Keep your cash on hand for marketing, hiring more staff, or covering those unexpected emergencies.

- Improve Efficiency: Upgrade to modern, energy-efficient models that cut down your utility bills and speed up prep times.

- Maintain Quality: Keep your food quality and safety top-notch with reliable, NSF-certified equipment.

- Scale Your Business: Add the gear you need to expand your menu, open a second location, or finally launch that catering service you've been dreaming of.

Financing bridges the gap between the kitchen you have and the kitchen you need to thrive. It converts a major capital expenditure into a manageable monthly operating expense, freeing you to focus on growth.

Beyond traditional loans and leases, you can also look into various non-dilutive funding options that bring in capital without forcing you to give up a piece of your business. This guide will give you a clear roadmap to upgrading your kitchen without breaking the bank.

Choosing Your Path: Equipment Loans vs. Leases

Trying to figure out financing restaurant equipment can feel like you're staring at a huge, complicated menu. But really, it boils down to one core choice: are you buying or are you renting? That single decision shapes how you manage your money and your assets down the road.

Think of an equipment loan like getting a mortgage for your oven. You make consistent payments over a fixed period, and with each payment, you own a little bit more of it. When the loan term is over, that beautiful convection oven is 100% yours. It’s a real asset on your books, boosting your restaurant's overall value.

On the flip side, an equipment lease is more like renting an apartment for your kitchen gear. Your monthly payments are lower, and you get the flexibility to swap it out for a newer, better model when your lease is up. The catch? You don't build any ownership, unless you've got a specific lease-to-own deal in place.

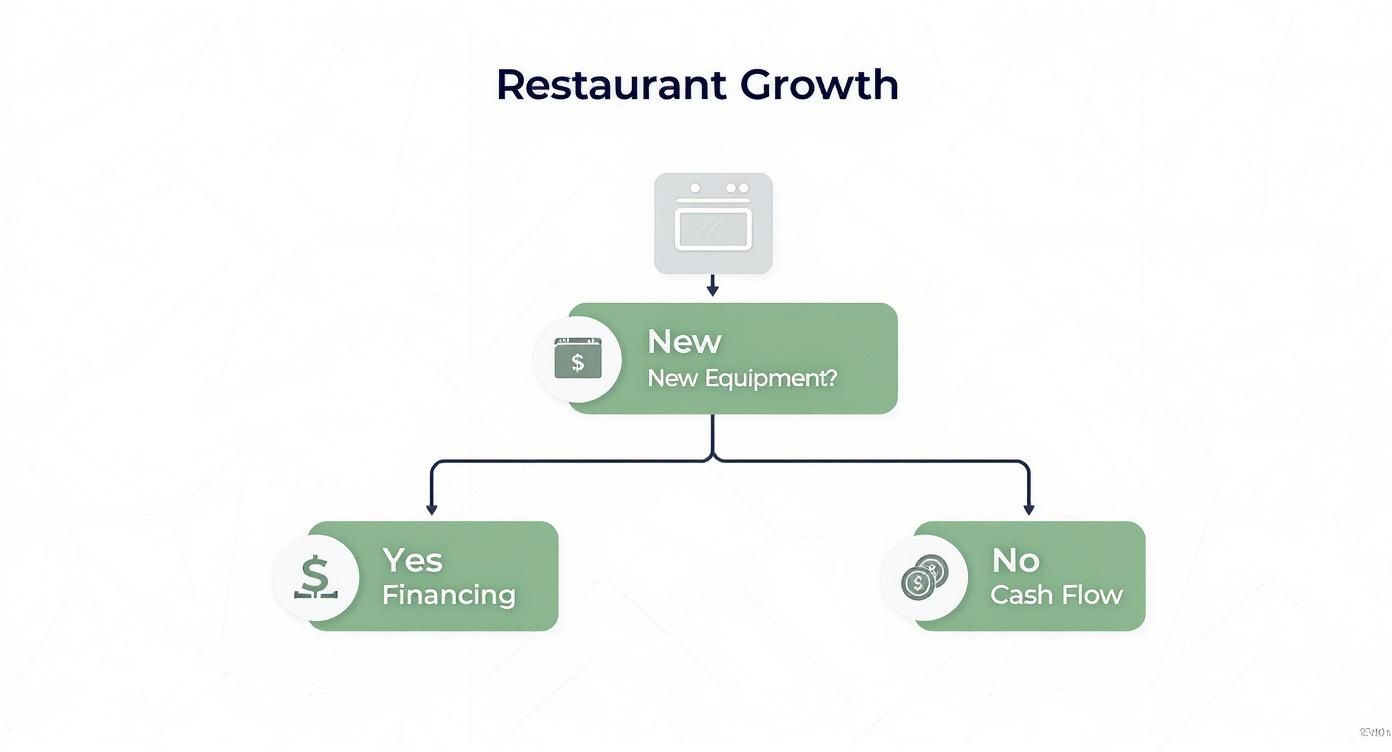

This visual decision tree helps simplify that first big choice every restaurant owner faces when they need new gear.

As the infographic shows, when you need new equipment, financing is usually the smartest way to get it. It lets you keep your cash free for all the other things that keep your restaurant running day-to-day.

Diving Deeper Into Equipment Loans

An equipment loan is as straightforward as it gets. You get a lump sum of cash to buy what you need, and you pay it back over time with interest. This is the perfect route for owners who see their equipment as a long-term investment and are ready to own it outright.

Here’s why a loan might be the right call:

- Full Ownership: Once it's paid off, that equipment is yours. You can sell it, customize it, or even use it as collateral for another loan in the future.

- Building Equity: Every single payment builds your stake in a real, tangible asset. That makes your restaurant's balance sheet look a whole lot stronger.

- Tax Advantages: You can often write off the equipment's depreciation and the interest you pay on the loan. That can lead to some serious tax savings.

Of course, there’s a trade-off. Loans usually demand a down payment and involve a tougher application process, making them a better fit for established spots with solid credit. For a more detailed breakdown, check out our guide on equipment leasing vs buying.

The Flexibility of Equipment Leases

Leasing is a fantastic option if you want to keep your kitchen decked out with the latest tech without locking yourself into ownership. It's all about access over assets.

A lease keeps your monthly overhead low and your kitchen modern. It’s a strategic move for managing cash flow, especially when you need equipment that requires frequent upgrades, like POS systems or specialty cooking appliances.

Leasing really shines in a few key areas:

- Lower Monthly Payments: Lease payments are almost always lower than loan payments. You're just paying for the value the equipment loses over the time you're using it, not its full sticker price.

- Minimal Upfront Cost: Many leases require little to no down payment, which is a lifesaver when you need to get expensive gear without emptying your bank account.

- Easy Upgrades: When the lease ends, you just hand the old equipment back and get the newest model. No fuss, no hassle.

The main downside? You don't own a thing at the end of the term. While some leases give you the option to buy the equipment, the total cost can sometimes add up to more than if you had just taken out a loan from the start.

Exploring Other Powerful Financing Tools

Beyond the classic loan-versus-lease debate, there are a few other powerful tools you can use to outfit your kitchen. These options are built for specific situations and can be a perfect fit depending on your needs.

Financing Options At A Glance

To make things a bit clearer, here’s a quick table breaking down the most common financing methods. This should help you see at a glance which path might align best with your restaurant's goals.

| Financing Type | Best For | Pros | Cons |

|---|---|---|---|

| Equipment Loan | Established businesses wanting to own assets long-term. | Full ownership, builds equity, tax benefits. | Higher payments, requires a down payment, stricter application. |

| Equipment Lease | Startups or businesses wanting the latest tech with low upfront costs. | Lower payments, minimal down payment, easy upgrades. | No ownership, can be more expensive long-term, mileage/usage limits. |

| SBA Loan | Businesses with strong plans that need favorable, long-term financing. | Low interest rates, long repayment terms, government-backed. | Slow approval process, requires extensive paperwork. |

| Vendor Financing | Businesses that need equipment quickly and value convenience. | Fast and convenient, often bundled with purchase, flexible terms. | Can have higher interest rates, limited to that vendor's equipment. |

| Business Line of Credit | Covering unexpected costs or seizing opportunities. | Ultimate flexibility, only pay interest on what you use, always available. | Variable interest rates, potential for overspending. |

This table is just a starting point. The real magic happens when you dig into the details and match the tool to the job.

A Closer Look at Your Options

SBA Loans are backed by the U.S. Small Business Administration, which makes lenders feel a lot more comfortable. For you, that usually means better terms, like lower interest rates and longer payback periods. They are a fantastic deal, but be prepared for a ton of paperwork and a longer wait.

Vendor Financing is offered right from the company selling you the equipment. This is often the path of least resistance—you can get your financing approved right at the point of sale. While it's incredibly convenient, always shop their rates around to make sure you're not paying a premium for that ease.

Business Lines of Credit work just like a credit card for your business. You get approved for a certain amount, and you can dip into it whenever you need to, only paying interest on the funds you actually use. This gives you amazing flexibility for surprise repairs or jumping on a great deal for used equipment.

Choosing the right financing is a big strategic decision. It all comes down to your cash flow, your growth plans, and where you see your restaurant in five or ten years. And there's a reason the financing market is so huge—the industry is valued at USD 1.34 trillion, and an incredible 82% of businesses use financing to get the equipment they need. You can find more of these insights from The Business Research Company.

The Essential Kitchen Equipment You Can Finance

Financing your restaurant equipment is one of the smartest ways to build a professional kitchen without tying up all your cash. It lets you spread the cost of those big-ticket items over months, which is a lifesaver for your cash flow.

In any commercial kitchen, stainless steel prep tables are the unsung heroes. They are the workhorses that handle everything from chopping and mixing to plating. Their durable, non-porous surfaces are crucial for maintaining high hygiene standards, resisting both stains and corrosion. Financing these tables turns a major purchase into a manageable monthly payment, keeping your working capital free for things like payroll and inventory.

Types of Stainless Steel Prep Tables

Choosing the right prep table can significantly boost your kitchen's efficiency. The key is matching the table's features to your specific workflow.

- Standard Work Tables: These are the most common and versatile. A simple flat-top stainless steel surface provides a large, open area perfect for general prep tasks like dicing vegetables, portioning meats, or assembling dishes.

- Tables with Undershelves: Adding a galvanized or stainless steel undershelf provides crucial storage space right where you need it. This keeps essential tools, containers, and small appliances organized and within arm's reach.

- Tables with Backsplashes: A backsplash prevents food and liquids from splashing onto walls, making cleanup easier and improving sanitation. They are ideal for placement against a wall, especially in wet prep areas.

- Mobile/Portable Tables: Equipped with casters, these tables offer flexibility. You can easily move them to different stations as needed or roll them out of the way for deep cleaning.

Always look for NSF certification to ensure any table meets public health and safety standards.

Specialized Prep Tables: Sandwich and Pizza Stations

For specific menu items, specialized prep tables are a game-changer. They combine prep space with refrigerated storage to streamline assembly and maintain food safety.

Sandwich/Salad Prep Tables

These units are designed for speed and efficiency in creating sandwiches, salads, and wraps.

- Refrigerated Rail: The top features a row of cold wells (pans) to hold perishable ingredients like deli meats, cheeses, and vegetables at a food-safe temperature (typically below 41°F).

- Cutting Board: A cutting board runs the length of the unit in front of the wells, providing an immediate workspace.

- Refrigerated Base: The cabinet below offers additional cold storage for backup ingredients, reducing trips to the main walk-in cooler.

A deli that upgraded to a 6-foot sandwich prep table saw its order completion time during the lunch rush improve by 20%.

Pizza Prep Tables

Built to handle the unique demands of pizza making, these tables optimize the entire process.

- Wide, Deep Surface: They often feature a wider surface, sometimes made of marble, which stays cool and prevents dough from sticking.

- Raised Refrigerated Rail: Similar to sandwich units, a raised rail holds all your toppings—sauce, cheese, pepperoni—within easy reach.

- Refrigerated Base: The base provides ample space for storing dough boxes and backup toppings.

A pizzeria was able to cut its prep time in half after upgrading to proper pizza prep tables. It’s a perfect example of how financing the right equipment directly boosts your efficiency.

For a more comprehensive list, check out our Commercial Kitchen Equipment Checklist.

Beyond the prep stations, you can finance just about every other key piece of equipment that powers your kitchen.

Other Equipment You Can Finance

Commercial cooking ranges, whether gas or electric, are the heart of the kitchen. Financing allows you to get a high-end model with powerful BTUs without the huge initial outlay.

Convection ovens are another popular item. Their fan-assisted heat can reduce cook times by up to 15%, which is a huge plus for baking and roasting.

You can also finance walk-in coolers and freezers. These units protect your most valuable asset—your ingredients—and let you buy in bulk to save money. And don't forget industrial dishwashers that can clean hundreds of plates an hour, ensuring you never run out of clean dishes during a rush.

When you're planning your financing, here are a few things to keep in mind:

- Map your equipment costs against your projected revenue.

- Try to align payment schedules with your slower seasons if possible.

- Always factor in maintenance and insurance costs when building your budget.

- The biggest benefit of financing is that it preserves your capital for day-to-day operations.

- It also gives you predictable monthly expenses, which makes financial forecasting much easier.

Each piece of equipment you finance is an asset. With flexible terms, you can often upgrade or replace it as your needs change. Think of financing as the key that unlocks the kitchen of your dreams today, not years from now.

- Reduce upfront costs

- Improve operational efficiency

- Preserve capital for growth

- Access top-tier brands and models

Ready to build out your kitchen and take your business to the next level? The best first step is to talk to a financing specialist who can help you find a plan that works for you.

Unlocking Hidden Tax Advantages with Financing

Choosing to finance your restaurant equipment goes way beyond just managing your cash flow. It's a savvy move for playing the tax game to your advantage. When you know how to navigate the tax code, financing stops being just a monthly payment and becomes a tool that can seriously lower your taxable income.

A lot of restaurant owners get hung up on the interest rate. But the real win is often buried in the tax deductions. By roping in your accountant early, you can turn a huge equipment purchase into a major financial victory when tax season rolls around. It’s all about making your financing pull double duty for you.

Section 179: The Immediate Write-Off

One of the best tools in the toolbox for any restaurant owner is Section 179 of the IRS tax code. Think of it as a deduction on steroids. Instead of slowly depreciating an asset over many years, Section 179 lets you deduct the full purchase price of qualifying equipment in the same tax year you start using it.

This is a complete game-changer. Let's say you finance a brand-new commercial oven for $50,000. Normally, you'd write off just a tiny piece of that cost each year. With Section 179, you can deduct the entire $50,000 from your gross income right away, which can slash your tax bill for that year.

The magic of Section 179 is immediate relief. It’s designed to encourage businesses to invest in themselves by letting them get the full tax benefit of a purchase now, not five years from now.

This instant deduction gives your cash flow a healthy boost, which ultimately lowers the real cost of your new equipment. While tax laws differ around the world, many countries have similar programs. For instance, the Australian Government's Instant Asset Write-Off works on a very similar principle and is a huge advantage for businesses down under.

Deducting Lease Payments as Operating Expenses

If you decide to lease your restaurant equipment instead of buying it with a loan, you tap into a different—but just as powerful—tax benefit. For most operating leases, your monthly payments are treated as standard operating expenses.

This means you can usually deduct the entire lease payment every single month. It's a clean, predictable way to lower your taxable income.

- Predictable Deductions: Forget complicated depreciation math. Lease payments are a simple, consistent expense you can write off.

- Off-Balance-Sheet Financing: Operating leases often don't show up as a liability on your balance sheet, which can make your business look financially healthier to other lenders.

- Simpler Accounting: Honestly, tracking lease payments is just plain easier than managing depreciation schedules for a kitchen full of equipment.

For example, if you lease a high-capacity ice machine for $300 a month, that adds up to $3,600 in deductible expenses you can claim over the year. This steady deduction makes financial planning easier and provides consistent tax savings.

Making Smart Financial Decisions

Getting a handle on these tax benefits is more important than ever as kitchens continue to modernize. In the United Kingdom alone, the restaurant equipment market is expected to grow at a 4.9% CAGR through 2035, driven by a booming hospitality sector. You can dig deeper into this trend over at Future Market Insights.

Knowing how to use tax codes like Section 179 or how to deduct lease payments lets you get the equipment you need without breaking the bank. The key is to have these conversations with your accountant before you sign on the dotted line. They can help you figure out which route—a loan or a lease—gives you the biggest tax win for your specific situation. A little planning upfront ensures your investment in new equipment is also a smart investment in your restaurant's bottom line.

A Step-By-Step Guide to the Application Process

Getting financing for your restaurant equipment can feel like a huge mountain to climb, but it’s really just a series of small, manageable steps. Think of it like a recipe—if you follow the instructions and get your prep work done, the final result will be a success. The secret is being organized and prepared, which is the fastest way to get the cash you need without hitting any snags.

The absolute first thing you have to do is get your financial house in order. Lenders need a crystal-clear snapshot of your restaurant's health and your track record with managing money. It’s not just about showing you’re profitable; it’s about proving you’re stable and have a smart plan for the future.

Step 1: Gather Your Essential Documents

Before you even think about talking to a lender, you need to pull together your financial toolkit. This is non-negotiable. Walking in with all your paperwork ready shows lenders you’re a serious, organized operator. Most financiers are going to ask for the same core documents, so you might as well get them ready now.

Here’s what you’ll need:

- Business Financial Statements: Your profit and loss (P&L) statement, balance sheet, and cash flow statement. Have the last two to three years ready.

- Personal and Business Tax Returns: Lenders will want to see at least two years of returns to get a full picture of your financial history.

- Bank Statements: Grab your last three to six months of business bank statements. This shows them your real-world, day-to-day cash flow.

- A Solid Business Plan: This is your chance to tell a story. Explain your restaurant's concept, who you serve, and exactly how this new equipment is going to help you make more money.

Think of your paperwork as the mise en place for your loan application. Having everything prepped and organized makes the whole process faster and smoother—just like in a well-run kitchen.

Step 2: Research and Select the Right Lender

Not all lenders are the same, and that’s especially true when you’re in the restaurant business. Some lenders live and breathe foodservice and understand its up-and-down cash flow cycles. Others use a one-size-fits-all approach that might not work for you. Finding a partner who actually gets your industry is a game-changer.

Start by looking at different types of lenders—traditional banks, credit unions, online financiers, and companies that only do equipment loans. Online lenders are often quicker to approve, but a bank might give you a better interest rate if you’ve been around a while and have great credit.

The key is to find a lender with experience in financing restaurant equipment. Ask them about their process, how long approvals usually take, and what kinds of terms they’ve given to other restaurants. Don’t be afraid to check reviews or ask for references to get a feel for their service and reliability.

Step 3: Complete and Submit the Application

Once you've picked a lender, it's time to fill out the application. Honesty and accuracy are everything here. Even tiny mistakes or numbers that don’t quite line up can throw up a red flag, causing delays or even getting you denied.

Before you click "submit," go over everything one last time:

- Check that all names, addresses, and tax IDs are perfect.

- Answer every question clearly and directly.

- Make sure you’ve attached all the right documents in the format they asked for.

Step 4: Navigate Underwriting and Approval

After your application is in, it heads to underwriting. This is where the lender’s team digs into your financials, credit history, and business plan to figure out the risk. They’re basically confirming that your restaurant can easily take on the new monthly payment.

Don’t be surprised if the lender comes back with a few more questions or asks for another document. When they do, respond as quickly and completely as you can to keep things moving. If you’re approved, you’ll get an official offer laying out the loan amount, interest rate, payment schedule, and any fees. Read every word of that offer before you sign to make sure it’s a deal that actually works for you.

How to Strengthen Your Application and Get Approved

Getting a lender to say 'yes' really boils down to one simple thing: proving your restaurant is a smart bet. It’s about more than just filling out paperwork. You need to paint a picture of a well-run business that’s ready to grow. A strong application tells a story of stability, profitability, and a clear plan for the future.

Your business plan is the foundation of that story. Don't treat it like a formality; it’s your chance to show lenders you’ve thought through every angle. You need to clearly connect the dots, explaining exactly how the new equipment will make you more money—whether that’s by speeding up service, expanding your menu, or cutting down on labor costs.

Fortify Your Financial Profile

Long before a lender even glances at your application, they're going to pull your credit. Both your personal and business credit scores are the first numbers they look at to figure out their risk. A higher score tells them you're financially responsible, and it dramatically boosts your odds of getting approved for financing restaurant equipment.

The first step is to pull your credit reports and check for any mistakes. You’d be surprised how often simple errors can drag down your score. After that, it's all about mastering the basics:

- Pay All Bills on Time: This is non-negotiable and the single biggest factor in your score. Late payments are a massive red flag.

- Keep Credit Utilization Low: On your business credit cards and lines of credit, try to use less than 30% of your available limit.

- Separate Business and Personal Finances: Always use a dedicated business bank account and credit card. It makes your books cleaner and shows lenders you’re serious.

A lender is betting on your ability to succeed. When you have a solid credit history and a detailed business plan, you turn that bet from a risky gamble into a calculated, confident investment on their part.

Present a Compelling Case for Funding

Good credit is a great start, but lenders also need to see how you're going to pay them back. This is where your financial projections and a willingness to share some of the risk become your most powerful arguments.

Show Them the Money (with Projections)

Pull together some realistic financial projections that clearly map out your restaurant's cash flow. Your goal is to show how the new monthly payment fits comfortably into your budget, without straining your operations.

For instance, if you're financing a new pizza prep table, project how many more pizzas you can crank out each hour. Then, translate that number into real dollars and cents of new revenue. If you're looking to keep those initial costs down, our guide on used stainless steel tables can help you build a financial model with a lower equipment price.

Make a Down Payment

Putting some money down—even when it's not required—is a game-changer. It signals to the lender that you have skin in the game, which instantly lowers their risk. A down payment of just 10-20% can make your application jump to the top of the pile and might even land you a better interest rate.

Build Lender Relationships Early

Don't wait until you're in a jam to start talking to lenders. Get to know your local bankers or connect with online financiers before you need the money. When they already know who you are and have a feel for your business, the whole process feels more like a conversation between partners, not a cold transaction.

Your Top Questions About Financing Restaurant Equipment

Restaurant owners often run into the same questions and hurdles when it's time to get funding for new kitchen gear.

Getting these common doubts cleared up from the start will help you make a much smarter decision for your business.

Knowing what lenders are looking for and how long things take can save you a ton of money and stress down the line.

Here are the questions we hear all the time:

- What credit score do I need to get approved?

- Can I even get financing for used equipment?

- How fast can I actually get the money?

- What are my options when a lease is over?

What Credit Score Do I Need?

Most lenders will want to see a personal credit score of 620 or higher.

But that's not the whole story. They'll also look at factors like how long you've been in business (time in business) and your annual revenue. A strong business can sometimes make up for a borderline score.

Some alternative lenders might work with lower scores, but you should expect to pay higher interest rates for that flexibility.

If you need to boost your score, the best things you can do are pay down existing credit card balances and make absolutely sure you don't have any late payments. It's also a good idea to check your credit report for any errors that could be dragging your score down.

Can I Finance Used Kitchen Equipment?

Yes, absolutely. Financing used equipment is incredibly common in the restaurant world, and lenders are very familiar with it.

Just know that they might offer you shorter repayment terms, since a used piece of gear obviously has less of a lifespan left than something brand new.

You should also expect the lender to require an inspection or appraisal to make sure the equipment is in good shape and worth what you're paying for it.

- The upside? A much lower purchase price saves you cash upfront.

- The structure: Shorter loan terms are designed to match the equipment’s remaining useful life.

- The catch: Sometimes, lenders charge slightly higher rates to offset their risk on an older asset.

How Quickly Will I Get the Funds?

This really depends on where you go. The new wave of online financiers can often approve an application in just 24–48 hours.

From there, the money can be in your bank account in just a few business days.

Your traditional bank or an SBA loan, on the other hand, is a much slower process. Be prepared for it to take several weeks, or even a couple of months, to get finalized.

Fast funding is a lifesaver when a critical piece of equipment breaks down and you can't afford any service disruptions.

If speed is what you need, look for lenders who specialize in the restaurant industry. They get the urgency and can often move things along much faster. Having all your financial documents ready to go will also shave a lot of time off the process.

What Happens at the End of a Lease?

When your lease term is up, you generally have three paths you can take.

You can simply return the equipment and walk away, no strings attached.

Another option is to renew the lease, often upgrading to a newer model.

Or, you can buy the equipment outright. Depending on your agreement, this could be at its "Fair Market Value" at the time, or it could be for just $1 if you signed a $1 Buyout Lease from the start.

Each option has a different total cost, so it's smart to run the numbers ahead of time. Compare the total cost of leasing and then buying versus just purchasing it from day one. This will help you pick the path that truly fits your budget and where you see your business going.

If we didn't cover your question here, our team is always ready to give you some one-on-one guidance on equipment financing.

Contact us to discuss financing options tailored to your kitchen's unique setup and menu.

Ready to get that kitchen upgrade without tying up all your cash?

Explore our top-quality stainless steel prep tables and refrigeration units today. Our financing plans are designed to keep your working capital free for what matters most—running your business.

You can browse all our financing resources and detailed buying guides online, then apply when you're ready.

Take the next step now with PrepTables.com.