How to Finance Restaurant Equipment The Smart Way

Financing your restaurant equipment isn't just about managing costs—it's a savvy move that lets you get the best tools for the job without draining your bank account. It means you can have high-performance gear, like a top-notch stainless steel prep table or efficient commercial refrigeration, from day one. This instantly boosts your kitchen's efficiency while keeping your cash free for day-to-day essentials like payroll and inventory.

You're essentially putting the best equipment to work for you right away, letting it help you generate revenue from the get-go.

Why Smart Financing Is Your Kitchen’s Secret Ingredient

Outfitting a kitchen, whether it's brand new or a much-needed upgrade, is a huge investment. Paying cash upfront might feel like the most responsible option, but it can seriously hamstring your business by tying up all your liquid assets. Think of financing not as taking on debt, but as a strategic play to grow your restaurant smarter and faster.

The biggest win here is preserving your working capital. Cash is the lifeblood of any restaurant; you need it for everything from buying produce to running a marketing campaign or handling an unexpected plumbing issue. Pouring all of that into equipment can leave you dangerously exposed. Financing, on the other hand, transforms a massive upfront hit into predictable, manageable monthly payments.

This strategy lets you get the right equipment for your kitchen, not just what you can afford to buy outright today. Instead of settling for a smaller, less efficient pizza prep table that creates a bottleneck during service, you can finance the perfect unit that streamlines your workflow and increases output from the moment it’s plugged in.

When you finance equipment, you're putting those assets to work immediately. They start generating revenue, often creating a return that’s bigger than the cost of the financing itself. It’s a classic case of making your money work for you.

Financing Options At a Glance

To make sense of it all, here's a quick breakdown of the most common financing methods for restaurant equipment. Each has its place, depending on your business's situation and goals.

| Financing Type | Best For | Typical Term Length | Ownership |

|---|---|---|---|

| Equipment Loan | Restaurants wanting to own equipment long-term and build equity. | 2-7 years | You own the equipment after the loan is paid off. |

| Equipment Lease | Businesses that want lower monthly payments or plan to upgrade equipment regularly. | 1-5 years | You don't own it; you can return it or buy it at the end of the term. |

| SBA Loans | Startups and established businesses needing favorable terms and lower interest rates. | Up to 10 years | You own the equipment. |

| Vendor Financing | New restaurants or those with less-than-perfect credit needing a quick, simple process. | 1-5 years | Varies by program; can be a loan or a lease. |

| Merchant Cash Advance | Businesses with high credit card sales needing fast cash, despite high costs. | 3-18 months | N/A (It's an advance, not a loan for a specific asset). |

Ultimately, the best choice depends on your specific financial picture and how you plan to use the equipment.

Turning Equipment Costs Into Growth Opportunities

Financing is a direct line to a faster return on your investment. Let's be honest, high-quality gear—whether it's a durable stainless steel prep table or an energy-efficient walk-in cooler—pays for itself over time. It does this through better productivity, less food waste, and even lower utility bills. If you wait to save up the cash, you're just delaying those benefits and leaving money on the table.

This approach is a game-changer for restaurants at every stage.

- For Startups: Financing is often the only realistic way to afford the professional-grade kitchen needed to even compete. It levels the playing field, allowing a new spot to operate like a well-oiled machine from the very beginning.

- For Existing Restaurants: It’s the perfect way to upgrade that aging oven, expand your menu capabilities, or improve your kitchen’s layout without choking your cash flow. It keeps you modern, efficient, and competitive.

At the end of the day, choosing to finance restaurant equipment is an investment in your kitchen’s future. It frees up your capital for the daily grind while giving your team the tools they need to knock it out of the park. Before you dive too deep, make sure you've covered all your other bases by reviewing this handy checklist for opening a restaurant.

Decoding Your Best Financing Options

Navigating the world of equipment financing can feel like trying to read a menu in a foreign language. Each option has its own unique flavor, and what works for a bustling downtown bistro might not be the right fit for a brand-new food truck. The key is to understand the core ingredients of each financing type so you can pick the one that best supports your restaurant's specific goals.

Choosing how to finance restaurant equipment isn't just a financial transaction. It's a strategic move that impacts your cash flow, tax liabilities, and ability to grow. Let's break down the most common paths restaurant owners take, complete with real-world scenarios to help you see where your business fits in.

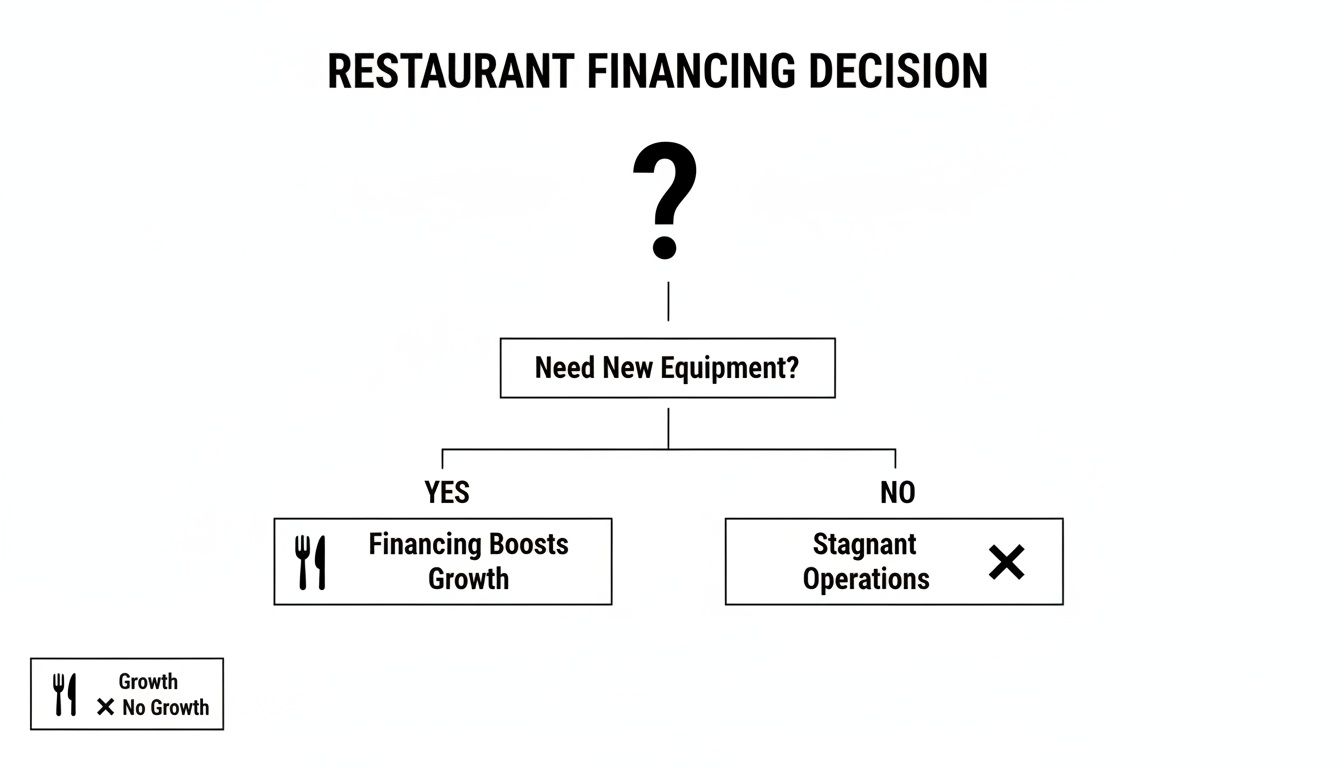

This decision-making process is critical, as investing in the right equipment is directly linked to operational efficiency and growth potential.

The flowchart above simplifies the choice: embracing financing leads to growth, while delaying equipment upgrades can lead to operational stagnation.

Traditional Bank Loans

This is the classic route. A traditional bank loan gives you a lump sum of cash to purchase your equipment, which you then repay over a set term with a fixed interest rate. Think of it as the prime rib of financing—reliable and well-understood.

These loans typically have the lowest interest rates, which is their main appeal. However, they also come with the strictest eligibility requirements. Banks want to see a solid business history, excellent credit, and detailed financial statements.

- Best For: Established restaurants with a proven track record of profitability and strong credit. A large catering company looking to buy a fleet of new warming cabinets would be a prime candidate.

- Drawback: The application process can be slow and document-heavy, making it less ideal for urgent equipment needs.

Equipment Leases

An equipment lease is more like renting than buying. You make monthly payments to use the equipment for a specific period. At the end of the term, you usually have the option to buy it, renew the lease, or return it for a newer model.

Leasing is incredibly popular in the restaurant industry because it requires a lower upfront cost and offers predictable monthly payments. This flexibility is perfect for new businesses or those who want to stay on the cutting edge of technology without the commitment of ownership.

For instance, a modern pizzeria might lease a high-tech pizza prep table with advanced refrigeration. After three years, they can swap it for the latest model with better energy efficiency. Making the right choice here is important, and you can explore the nuances in our guide on equipment leasing vs. buying.

Leasing allows you to preserve your precious cash for other vital business needs, like marketing or inventory. It keeps your balance sheet looking lean because the equipment isn't listed as a long-term asset or liability.

Merchant Cash Advances (MCAs)

A Merchant Cash Advance isn't technically a loan. Instead, a lender gives you an upfront sum of cash in exchange for a percentage of your future credit card sales. Repayment is automatic and taken directly from your daily card transactions.

The biggest advantage of an MCA is speed. You can often get funded in a day or two with minimal paperwork, which is a lifesaver when an essential piece of equipment suddenly breaks down. This makes it a go-to option for restaurants with high credit card sales volume and an urgent need for cash.

However, this convenience comes at a high cost. MCAs have much higher effective interest rates than traditional loans, so they should be used cautiously and primarily for short-term emergencies.

SBA Loans

Backed by the U.S. Small Business Administration, SBA loans are offered by partner lenders and come with favorable terms, including low interest rates and long repayment periods. They are designed to help small businesses thrive.

SBA loans are fantastic for significant investments, like a complete kitchen overhaul or outfitting a brand-new restaurant. The government guarantee reduces the risk for lenders, making them more willing to offer great terms.

The downside is similar to bank loans—the application process is notoriously long and requires a mountain of paperwork. But for those who qualify and have the patience, the benefits are hard to beat.

Vendor or Manufacturer Financing

Many equipment suppliers, including us at PrepTables.com, offer their own financing programs. This is often one of the most convenient ways to finance restaurant equipment because you handle the purchase and the financing all in one place.

Vendor financing is often tailored specifically to the equipment you're buying. It can be structured as a loan or a lease and is generally easier to qualify for than a bank loan, making it a great option for new businesses or those with less-than-perfect credit.

This direct-from-the-source financing is part of a massive, growing industry. Envision scaling your deli with undercounter freezers that preserve meats flawlessly, amid a restaurant equipment sector rocketing from $92.89 billion in 2024 to $206.07 billion by 2035. This growth is fueled by an increasing demand for quality food, where cooling and prep tables are among the fastest-growing segments. Globally, equipment leases are projected to become a $54.92 billion market by 2029, as restaurants from food trucks to luxury dining establishments invest in efficiency.

Preparing Your Application for a Fast Approval

Getting a "yes" on your application to finance restaurant equipment really boils down to one thing: preparation. Lenders are in the business of assessing risk, and a sharp, well-organized application package tells them you're a serious operator who has their act together.

Think of it as your restaurant's financial resume. You're making a first impression, and you want it to be a good one. Coming to the table with all your documents ready not only gets you an answer faster but also seriously bumps up your chances of approval. A lender who sees a complete, professional application knows you’re ready for the responsibility.

Assembling Your Essential Documents

Before you even think about filling out a form, get your paperwork in order. Tucking these away in a digital folder will make the whole process a breeze.

- A Well-Defined Business Plan: This is non-negotiable for startups. If you're an existing spot, it should detail your growth plans. It needs to have realistic financial projections, a clear breakdown of your concept, and an honest look at your target market.

- Personal and Business Tax Returns: Lenders will almost always ask for the last two to three years of returns. This gives them a clear window into your financial history and profitability.

- Recent Bank Statements: Plan on providing three to six months of business bank statements. It's the simplest way for a lender to verify your cash flow and see how your operation is doing day-to-day.

- Legal Business Documents: Have your business license, articles of incorporation (or LLC docs), and any key permits handy. This is just basic proof that your business is legitimate and operating by the book.

Having all this ready from the start saves you from the frustrating email chains that can stall a decision for days, or even weeks.

Crafting a Credibility-Building Application

It’s not just about submitting the right papers; how you present your request makes a huge difference. Your goal is to tell a story that convinces the lender you're a reliable partner who will make their payments on time.

A huge piece of that puzzle is the equipment quote itself. Lenders want to see you're making a smart investment that will actually help your restaurant succeed, not just buying a shiny new toy.

A detailed equipment quote is more than just a price—it's a statement of intent. Specifying an NSF-certified stainless steel prep table with a 16-gauge top and a 700 lb load capacity shows you understand quality and are investing in equipment built to last in a demanding commercial environment.

That kind of detail shows you're thinking about the long-term value and ROI. It’s way more convincing than a generic quote for a "prep table," and it tells the lender their investment is funding a quality asset.

Insider Tips for a Stronger Submission

Want to really set your application apart? Go the extra mile. A few simple steps can improve your odds and maybe even land you better terms.

- Write a Brief Executive Summary: A simple one-page cover letter can work wonders. In a few paragraphs, explain who you are, what your restaurant is all about, what you need to buy, and exactly how it will make you more money. For example, "This new pizza prep table will allow us to increase our lunch service output by 30%."

- Clean Up Your Credit: Before you apply, pull both your personal and business credit reports. Look for errors to dispute and pay down some high-balance cards if you can. A few extra points on your credit score can make a big difference in the offers you get.

- Provide a Clear Use of Funds: Don't just list the equipment; explain its job. For instance, "The undercounter freezer will be dedicated to our house-made ice cream program, which currently accounts for 15% of our dessert sales and is projected to double with this expansion."

By taking these steps, you're not just filling out a form. You're building a compelling business case that shows a clear path to growth. You're making it easy for any lender to get behind your vision.

Let's bring this down from the clouds and talk about the actual steel and refrigeration that keeps your kitchen humming. Theory is great, but it's more helpful to connect financing concepts to the specific gear your team relies on every single day.

Different pieces of equipment come with their own financial quirks, and figuring those out is key to choosing the smartest way to pay for them.

Before you start shopping, it's a good idea to get a handle on how to calculate capital spending. This isn't just busywork; it's a crucial step that helps you justify the expense and see the kind of return you can expect from your investment.

The Versatile Stainless Steel Prep Table

Every kitchen's unsung hero is the stainless steel prep table. They are the true backbone of your workflow. Compared to a new oven or walk-in cooler, they're relatively low-cost, but their effect on your kitchen's efficiency is huge.

Because they’re built to last, these tables are a great candidate for an outright purchase or a straightforward equipment loan.

You're not just buying one kind of table, either. The variety is massive, and each one solves a different problem.

- Standard Work Tables: These are the classics. A simple, flat surface for all your chopping, mixing, and plating. They usually have an undershelf for extra storage, and you can often bundle a few of them into a larger equipment financing package.

- Tables with Integrated Sinks: This is a smart move for saving steps. Combining a prep surface with a sink keeps the food washing and prep process in one spot, which is a lifesaver in a tight kitchen.

- Mobile or Caster Tables: Putting wheels on a prep table gives you amazing flexibility. You can shift your kitchen layout around for a special event or just make deep cleaning a whole lot easier.

- Wall-Mounted Shelves and Tables: For kitchens where floor space is at a premium, these are brilliant. They provide extra prep or storage space without creating another obstacle for staff to navigate.

When you finance restaurant equipment like a quality, NSF-certified stainless steel table, you're buying a long-term asset. I've seen well-maintained tables last for decades, delivering value long after the final loan payment is made.

The global market for restaurant equipment was valued at $3.88 billion in 2024 and is expected to climb to $5.58 billion by 2029. That growth is all about the demand for durable, hygienic gear that meets today's tough food safety standards—exactly what a good prep table provides. It shows that making a smart financing move on essential items like these is a solid bet for your restaurant's future.

Specialized Refrigerated Prep Tables

Now we’re getting into more complex, specialized units like sandwich and pizza prep tables. For certain restaurants, these aren't just helpful; they're absolute game-changers. They combine your workspace, refrigerated ingredient wells, and under-counter cold storage into one hyper-efficient station.

These units cost a lot more than a standard table and have complex parts like compressors and cooling systems. That makes them perfect for leasing. A lease gets you a top-of-the-line model with a much lower upfront cost and a predictable monthly payment.

Sandwich and Salad Prep Tables

If you run a deli, café, or salad bar, these tables are the heart of your operation. They keep your lettuce, tomatoes, and meats perfectly chilled and right where your staff needs them, which makes a huge difference during a chaotic lunch rush. They typically feature a cutting board running the length of the unit and a refrigerated top section to hold food pans.

Think about a sandwich shop owner who finances a new refrigerated prep table. The monthly lease payment is just another line item, but the return on that investment is crystal clear.

- Faster Service: If you can shave just 30 seconds off each order, you can serve dozens more customers during your busiest hours.

- Better Workflow: A good layout means less running around for your staff, which reduces fatigue and boosts morale.

- Less Food Spoilage: Keeping ingredients at the right temperature cuts down on waste, which directly helps your food cost.

Often, the money you save from increased efficiency and reduced waste more than covers the monthly lease payment. From day one, that piece of equipment starts making you money. To get more ideas on the right gear, take a look at our guide to essential commercial kitchen equipment.

Pizza Prep Tables

It's the same story for any pizzeria—a pizza prep table is non-negotiable. These units have a wide, refrigerated rail built to hold all your topping pans at a safe, cool temperature. The workspace is often a marble or stone slab, which is perfect for stretching dough and stays naturally cool. Below, you’ll find refrigerated cabinets designed to hold dough boxes.

Pizza-making is a high-volume, fast-paced business, so the efficiency you get from a dedicated prep table is massive. By leasing a high-capacity unit, a pizzeria can crank out more orders without sacrificing quality, directly boosting revenue. Financing specialized equipment like this isn't just about getting a new toy; it's about investing in your restaurant's ability to grow.

Unlocking Tax Benefits and Negotiating Better Terms

Getting your financing approved is a huge win, but don't pop the champagne just yet. Now the real work begins: making sure that financing works as hard for you as possible. This is where you can turn a good deal into a great one, finding savings that pad your bottom line for years.

A little financial savvy goes a long way. By understanding the tax code and knowing how to negotiate, you can turn a major expense into a powerful strategic advantage for your restaurant.

Demystifying Your Tax Advantages

When you buy equipment—whether with cash or a loan—you’re also buying a powerful tool to lower your taxable income. The IRS gives you a few ways to do this, but a couple really stand out for restaurant owners.

The Section 179 deduction is a game-changer. It lets you deduct the entire purchase price of qualifying equipment in the same year you put it to use. So, instead of slowly depreciating that $10,000 pizza prep table over five or seven years, you could potentially write off the whole $10,000 right now.

It’s also crucial to understand how bonus depreciation works when you're adding new assets. This is another fantastic way to accelerate your tax savings and reduce what you owe in that first year.

Leasing, on the other hand, offers a simpler tax benefit. Since you don't actually own the equipment, your monthly payments are usually treated as regular operating expenses—just like your rent or utility bills. This means you can typically deduct the full amount you pay each year, which makes for very clean and predictable accounting.

Actionable Negotiation Tactics That Work

Once you have a few financing offers on the table, it's go-time. Never, ever accept the first offer. Lenders fully expect you to shop around, and that simple act gives you the leverage you need to get the best possible deal.

Start by getting quotes from at least three different lenders. This simple step creates competition and puts you in the driver's seat. When you start comparing the offers, remember to look past the interest rate.

The interest rate is only one part of the story. You must calculate the Total Cost of Borrowing (TCB), which includes all fees, closing costs, and interest over the entire life of the loan. A loan with a slightly lower rate but high upfront fees can end up costing you more.

Here are the non-negotiable questions you need to ask every lender to make sure you’re getting a transparent, fair deal:

- What are all the fees involved? Get specific. Ask about origination fees, application fees, or any other “processing” charges.

- Is there a prepayment penalty? If your restaurant has a killer year, you should have the freedom to pay off your loan early without getting dinged for it.

- What are the end-of-lease options? For leases, you need to know the buyout price, renewal terms, and return conditions right from the start. No surprises later.

Let’s put this in perspective. The restaurant equipment market is projected to hit $10.2 billion by 2035, a boom driven by operators investing in smart, efficient gear to meet demand. Imagine you’re outfitting a food truck and eye a $5,000 refrigerated prep unit. That single piece of equipment could boost your workflow efficiency by up to 30%. Nailing the financing negotiation means you get to that ROI much, much faster.

By focusing on these tax strategies and negotiation tactics, you’ll do more than just buy equipment—you’ll be making a smart investment in your restaurant’s long-term success.

Common Questions About Financing Restaurant Equipment

Jumping into the world of equipment financing always brings up a lot of questions. Getting clear, straightforward answers is what helps you move forward with confidence and make choices that will serve your restaurant well for years to come.

We’ve pulled together some of the most common questions we hear from restaurant owners when they decide to finance restaurant equipment. Think of this as your quick-reference guide for practical insights.

What Credit Score Do I Need?

Your credit score is a big piece of the puzzle, but the "magic number" can vary quite a bit. There isn't one single score that opens all the doors, as every lender and financing type plays by slightly different rules.

For traditional bank loans and SBA loans, lenders are generally looking for a strong personal credit score—often 680 or higher. These options offer the best rates and terms out there, so naturally, they have the toughest requirements.

Online lenders and equipment financing companies tend to be more flexible. They might work with applicants who have scores in the low-to-mid 600s. Merchant cash advances have the most relaxed credit requirements, sometimes approving owners with scores as low as 500, but that flexibility comes at a much higher cost.

It's a simple truth: a higher credit score doesn't just improve your odds of getting approved, it unlocks better interest rates and more favorable terms. Even a few points can mean saving a lot of money over the life of the loan.

Can I Finance Used Restaurant Equipment?

Yes, absolutely! Financing used equipment is a smart strategy for many restaurant owners trying to make their budget go further. Grabbing a pre-owned stainless steel prep table or a commercial freezer can save you a serious chunk of change upfront.

But not every lender is eager to finance used gear. Here’s what you should know:

- Lender Hesitation: Some traditional banks get a little nervous about financing used equipment. It’s harder for them to pin down its value, and they worry about its shorter lifespan.

- Specialized Lenders: On the other hand, many online and equipment-specific lenders are completely comfortable financing used equipment. They know the restaurant industry and understand that a well-maintained piece of gear is a great value.

- The Pros: The biggest win here is the cost savings. You can get your hands on high-quality, durable equipment for a fraction of what you'd pay for it new.

- The Cons: You’ll likely face shorter financing terms and potentially a higher interest rate to cover the lender's risk. Plus, you have to be prepared for the possibility of higher maintenance costs down the road.

If you're going after financing for used equipment, just be ready to provide all the details about the item—its age, condition, and where you're buying it from.

What Is the Real Difference Between a Loan and a Lease?

This is one of the most common points of confusion, and getting the difference is crucial for making the right call for your restaurant's finances. It really boils down to ownership and long-term cost.

With an equipment loan, you're borrowing money to buy an asset. You make payments covering principal and interest, and when the term is up, you own that piece of equipment outright. It goes on your balance sheet as an asset, and you can claim depreciation on your taxes.

With an equipment lease, you're essentially renting the equipment for a set amount of time. Your monthly payments are usually lower than loan payments because you’re only covering the equipment's depreciation during the lease, not its entire value. At the end of the term, you typically have the option to return it, sign a new lease, or buy it for whatever it's worth at that point.

Here's an easy way to think about it: a loan is your path to ownership, while a lease is paying for the use of the equipment.

How Quickly Can I Get Approved?

The time it takes to get from application to funding can be wildly different depending on the financing path you choose. Knowing what to expect can save you a ton of stress.

- Online Lenders & MCAs: These are the sprinters of the financing world. You can often fill out an application in minutes and have a decision—and sometimes the cash—in your account within 24 to 48 hours. They are built for pure speed.

- Vendor & Equipment Financiers: This process is also pretty quick, often wrapping up in just a few business days. Since they live and breathe equipment financing, their process is streamlined and efficient.

- Traditional Banks & SBA Loans: These are the marathon runners. The application is much more involved and requires a mountain of paperwork. Getting an approval can take anywhere from several weeks to a couple of months.

Bottom line: if your walk-in cooler dies today, an SBA loan isn't going to help you. But if you’re planning a full kitchen overhaul in six months, its great terms are definitely worth the wait.

At PrepTables.com, we understand that the right equipment is the foundation of an efficient kitchen. Explore our extensive selection of NSF-certified stainless steel work tables, refrigerated prep stations, and commercial cooking equipment to find the durable, high-performance gear your restaurant deserves. https://preptables.com